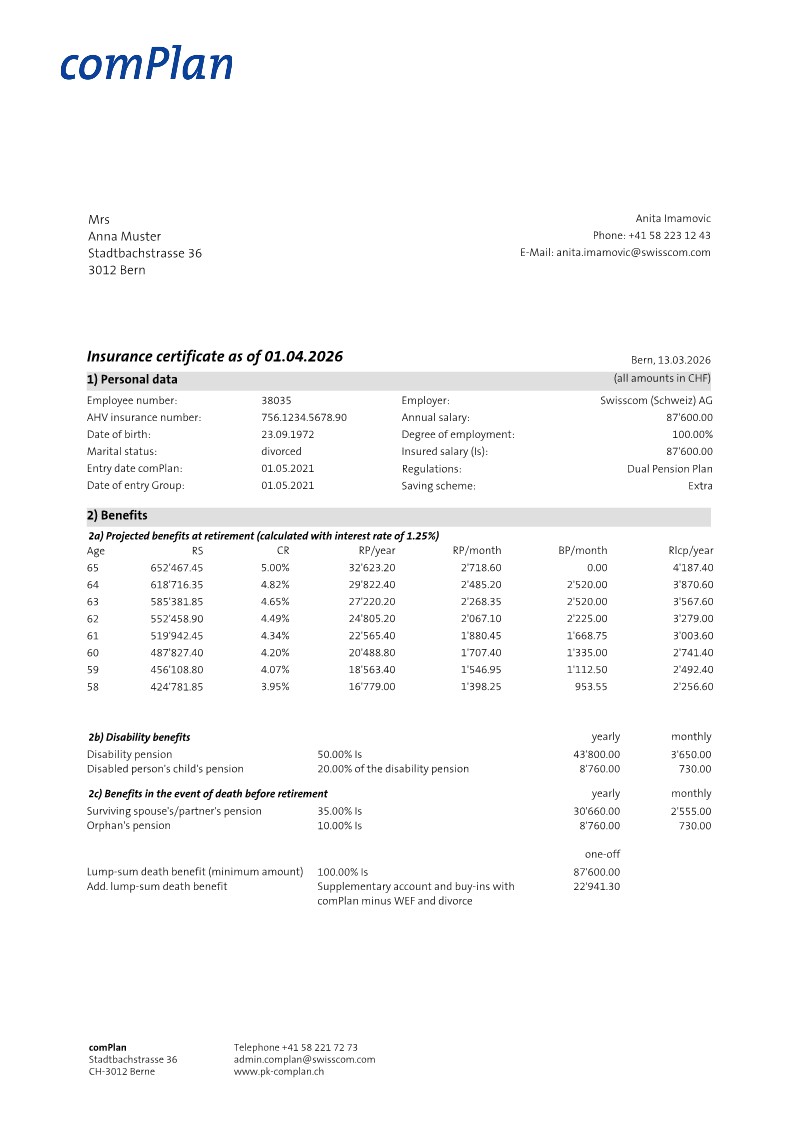

Insurance certificate as of: All calculations are based on the date shown.

Insurance certificate as of: All calculations are based on the date shown.

Salary: At comPlan, the insured salary (vL) corresponds to the basic salary plus the performance-related component payable if the target is met in full (annual salary)

Salary: At comPlan, the insured salary (vL) corresponds to the basic salary plus the performance-related component payable if the target is met in full (annual salary)

Projected benefits on retirement: The estimated balances and benefits shown are calculated based on current figures (insured salary, BVG minimum interest rate, conversion rate and existing retirement savings)

Projected benefits on retirement: The estimated balances and benefits shown are calculated based on current figures (insured salary, BVG minimum interest rate, conversion rate and existing retirement savings)

RS: Retirement assets

CR: Conversion rate

RP/year: Retirement pension per year

RP/month: pension per month

BP/month: AHV bridging per month

Rlcp/year: Retirement child's pension per year

RS: Retirement assets

CR: Conversion rate

RP/year: Retirement pension per year

RP/month: pension per month

BP/month: AHV bridging per month

Rlcp/year: Retirement child's pension per year

AHV bridging pension: In the event of early retirement, where the employee has been employed full-time for at least 10 years within the Swisscom Group, the employer will provide a one-off payment of up to CHF 80,100 to fund the AHV bridging pension. The amount is reduced by 1/120 for each month missing. The corresponding amount, which is paid monthly until the reference age, is shown in this column.

AHV bridging pension: In the event of early retirement, where the employee has been employed full-time for at least 10 years within the Swisscom Group, the employer will provide a one-off payment of up to CHF 80,100 to fund the AHV bridging pension. The amount is reduced by 1/120 for each month missing. The corresponding amount, which is paid monthly until the reference age, is shown in this column.

Disability benefits:

Disability pension: This is determined according to the degree of disability. The pension listed here corresponds to 100% disability.

Disability child’s pension: This is additionally paid to the disability pensioner for each child up to the age of 18. If the child is still in education or is at least 70% disabled, the entitlement continues until the child reaches the age of 25.

Disability benefits:

Disability pension: This is determined according to the degree of disability. The pension listed here corresponds to 100% disability.

Disability child’s pension: This is additionally paid to the disability pensioner for each child up to the age of 18. If the child is still in education or is at least 70% disabled, the entitlement continues until the child reaches the age of 25.

Death benefits:

Spouse’s pension/civil partner’s pension: If an insured person dies, the surviving spouse/life partner is entitled to a spouse's/life partner's pension if he/she is responsible for the maintenance of one or more children or has reached the age of 40 and was married to the deceased person for at least 5 years or lived together continuously in the same household (with the same official place of residence) and has submitted a declaration of beneficiaries. Entitlement to the civil partner’s pension only applies if the partnership has been registered with comPlan via a declaration of beneficiaries. This must be submitted to comPlan before retirement and before death.

Orphan’s pension: This is paid until the child reaches the age of 18. If the child is still in education or at least 70% disabled, entitlement continues until they reach the age of 25.

Death benefits:

Spouse’s pension/civil partner’s pension: If an insured person dies, the surviving spouse/life partner is entitled to a spouse's/life partner's pension if he/she is responsible for the maintenance of one or more children or has reached the age of 40 and was married to the deceased person for at least 5 years or lived together continuously in the same household (with the same official place of residence) and has submitted a declaration of beneficiaries. Entitlement to the civil partner’s pension only applies if the partnership has been registered with comPlan via a declaration of beneficiaries. This must be submitted to comPlan before retirement and before death.

Orphan’s pension: This is paid until the child reaches the age of 18. If the child is still in education or at least 70% disabled, entitlement continues until they reach the age of 25.

Lump-sum death benefit:

The surviving dependants are entitled to a death benefit, irrespective of inheritance law, in accordance with the following exhaustive and unalterable order of priority:

The spouse, or in their absence

The beneficiary partner, having shared a household for the last 5 years (no need for the same official residence) or persons substantially supported by the insured person (excluding a divorced spouse); in their absence

All children of the deceased (in equal shares)

The death benefit for these persons amounts to the retirement savings available at the time of death (see section 6) minus all pension payments triggered by the death; however, at least 100% of the last insured salary.

Additional death benefit: In the absence of all the aforementioned beneficiaries, entitlement to any additional death benefit lies with the following, unalterable order of priority:

The parents (in equal shares); in their absence

The siblings (in equal shares).

Lump-sum death benefit:

The surviving dependants are entitled to a death benefit, irrespective of inheritance law, in accordance with the following exhaustive and unalterable order of priority:

The spouse, or in their absence

The beneficiary partner, having shared a household for the last 5 years (no need for the same official residence) or persons substantially supported by the insured person (excluding a divorced spouse); in their absence

All children of the deceased (in equal shares)

The death benefit for these persons amounts to the retirement savings available at the time of death (see section 6) minus all pension payments triggered by the death; however, at least 100% of the last insured salary.

Additional death benefit: In the absence of all the aforementioned beneficiaries, entitlement to any additional death benefit lies with the following, unalterable order of priority:

The parents (in equal shares); in their absence

The siblings (in equal shares).

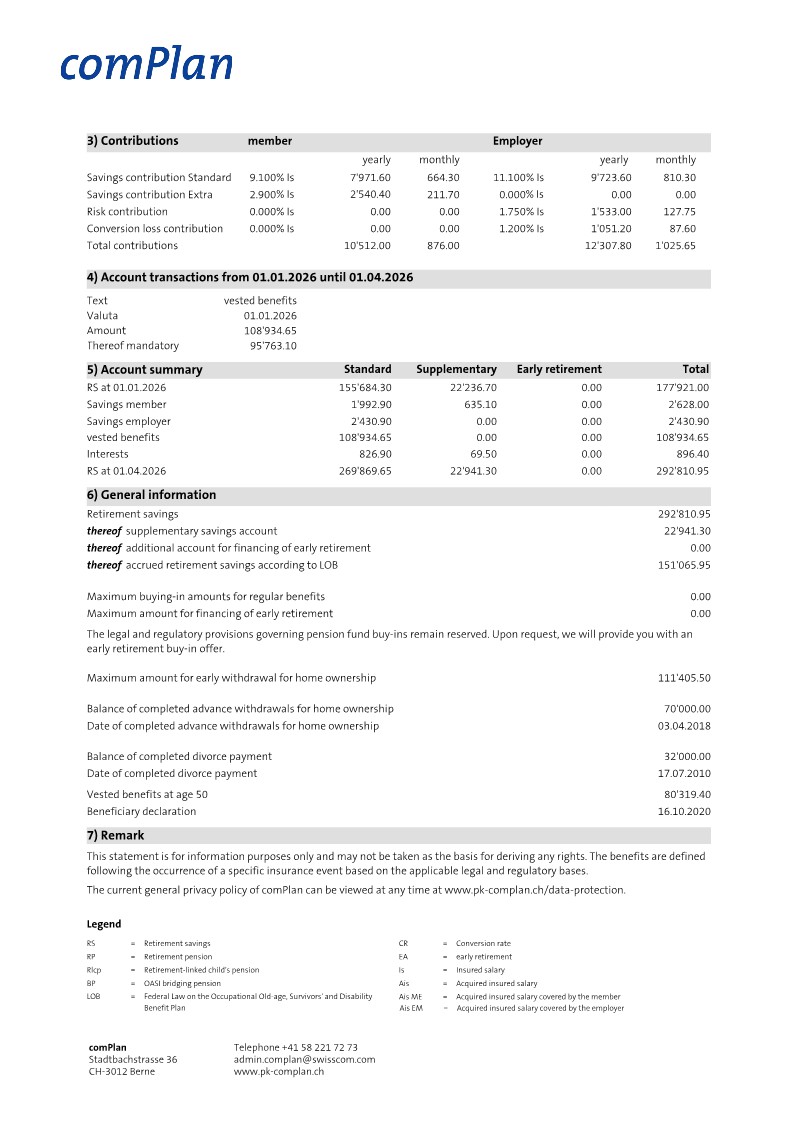

Contributions: At the start of the following month, choose between the ‘Standard’, “Plus” or ‘Extra’ savings options. You can find further information on this in the pension scheme regulations.

Contributions: At the start of the following month, choose between the ‘Standard’, “Plus” or ‘Extra’ savings options. You can find further information on this in the pension scheme regulations.

Savings contributions: Under the ‘Standard’ savings contribution scheme, the employer pays savings contributions of at least the same amount as the employee. The contribution levels are graded according to age categories; further details can be found in the pension scheme regulations.

Employees have the option of paying additional, higher savings contributions under the “Plus” and ‘Extra’ categories, thereby accumulating more capital.

Risk contributions: Risk contributions are paid in full by the employer and are used to fund benefits in the event of death or disability.

The contribution to cover the loss of the conversion rate is also financed exclusively by the employer.

Savings contributions: Under the ‘Standard’ savings contribution scheme, the employer pays savings contributions of at least the same amount as the employee. The contribution levels are graded according to age categories; further details can be found in the pension scheme regulations.

Employees have the option of paying additional, higher savings contributions under the “Plus” and ‘Extra’ categories, thereby accumulating more capital.

Risk contributions: Risk contributions are paid in full by the employer and are used to fund benefits in the event of death or disability.

The contribution to cover the loss of the conversion rate is also financed exclusively by the employer.

Account movements: The deposits and withdrawals made during the calendar year (or, in the case of the pension statement as at 1 January of the previous year) are shown in this section, so that changes in the retirement savings can be traced.

Account movements: The deposits and withdrawals made during the calendar year (or, in the case of the pension statement as at 1 January of the previous year) are shown in this section, so that changes in the retirement savings can be traced.

Account statement

Standard: This shows the standard savings contributions and account movements, including interest.

Additional savings: Records the savings contributions for the Plus and Extra savings plans.

VP account: Records contributions made towards early retirement.

Account statement

Standard: This shows the standard savings contributions and account movements, including interest.

Additional savings: Records the savings contributions for the Plus and Extra savings plans.

VP account: Records contributions made towards early retirement.

General information: Here you will find general information about your retirement savings, as well as an overview of any additional options available to you or withdrawals you have made.

General information: Here you will find general information about your retirement savings, as well as an overview of any additional options available to you or withdrawals you have made.

BVG retirement savings: The difference compared with the statutory retirement savings highlights the difference in benefits offered by comPlan compared with the minimum legal requirements.

BVG retirement savings: The difference compared with the statutory retirement savings highlights the difference in benefits offered by comPlan compared with the minimum legal requirements.

Maximum purchase amount for standard benefits: This figure corresponds to the difference between the maximum possible retirement savings and the actual amount held.

Maximum purchase amount for standard benefits: This figure corresponds to the difference between the maximum possible retirement savings and the actual amount held.

Maximum possible early withdrawal for home ownership: To finance home ownership, your current retirement savings (= termination benefit) are available until you reach the age of 50. If you are over the age of 50, you may withdraw no more than the greater of the following amounts:

– the termination benefit at the age of 50 or

– 50% of the termination benefit at the time of the early withdrawal.

The minimum amount for the early withdrawal is CHF 20,000.

Further provisions and information on home ownership support can be found in the separate brochure.

Balance of previous early withdrawals for home ownership: Once an early withdrawal has been made, a further early withdrawal is only possible again after a period of 5 years has elapsed.

Maximum possible early withdrawal for home ownership: To finance home ownership, your current retirement savings (= termination benefit) are available until you reach the age of 50. If you are over the age of 50, you may withdraw no more than the greater of the following amounts:

– the termination benefit at the age of 50 or

– 50% of the termination benefit at the time of the early withdrawal.

The minimum amount for the early withdrawal is CHF 20,000.

Further provisions and information on home ownership support can be found in the separate brochure.

Balance of previous early withdrawals for home ownership: Once an early withdrawal has been made, a further early withdrawal is only possible again after a period of 5 years has elapsed.

Beneficiary Declaration:

If a declaration has already been submitted, the relevant information can be viewed here.

Beneficiary Declaration:

If a declaration has already been submitted, the relevant information can be viewed here.